The Great Compression and the Currency of Belief

Venture Capital Liquidity Tricks and Other Delusions

The Physics of Bullshit

In 2021, venture capital broke its own math. $356B deployed1. Half the required winners and twice the confidence.

The Winner Constant2 set the mathematical leash: for every $1 billion in capital deployed, you need at least 0.17 mega-winners (>$5B exits) to keep the dream alive. When the ratio falls below that, paper marks begin to resemble Papiermarks, the currency of a previous delusion.

VCs responded the only way they know how: by doubling down. They kept shoving money into anything with a pulse and a pitch deck until the world was choking on unicorns: 1,630 worth more than $1B3 and 211 worth over $5B4. While preceding years cooled off, there’s been almost $1.6T of capital deployed into startups since 20181. Rarity has become commoditized.

You can inflate valuations with cash, but you can’t manufacture exits. Each oversized round just kicks the can closer to late-stage reality, where stories run headfirst into math. The fantasy always ends the same way: growth funds inheriting startups that can’t grow and founders discovering that public markets still require reality.

A system can tolerate belief as long as belief is cheaper than truth. In 2025, the only asset growing faster than AI is storytelling.

The Great Compression

The end of excess comes quietly when there’s nothing left to sell.

Portfolios age, exits dry up. DPI becomes a forgotten acronym. Cambridge Associates reported that VC funds called 1.5x5 more capital than they distributed in 2024, the lowest distribution yield in a decade.

There are buyers on paper, just none with conviction. So funds improvise. Continuation vehicles, extensions, secondary sales at valuations everyone winks at.

That’s stage one: manufacture time, reshuffle paper, pretend liquidity is a matter of willpower.

Stage two begins when LPs stop nodding. They want cash, not creativity. Letters get longer; language gets softer. “We’re prioritizing durable value.” “We’re pacing exits responsibly.” Every sentence is a way to buy another quarter.

Partner meetings start sounding like therapy sessions. LP calls turn into weather reports about market headwinds. Nobody admits the problem, because admitting it would make it real.

Stage three is when denial hardens into faith. The same language used to mask stagnation becomes doctrine. Efficiency turns into morality. Patience turns into policy. Eventually, pretense gives way to belief.

Venture stops promising exponential outcomes and starts preaching operational virtue. Decks fill with “durability,” “capital efficiency,” and “responsible growth.” It’s the same machine with the optics repackaged as sermons.

Funds need to deploy or die. LPs read the marks as validation, not inflation. Everyone agrees to call it maturity because the alternative is admitting paralysis.

When capital stops clearing, belief becomes the medium of exchange.

The Human Layer

When returns shrink, stories inflate. It’s emotional monetary policy.

Founders sell conviction to rooms that need belief. GPs sell control to rooms that need calm. LPs believe because disbelief would force a markdown. Is it lying if everyone believes the lie? The entire system is now a closed loop where the founder with single-digit growth but “AI-native” branding presents to a GP who knows the truth, but who needs to push the mark to an LP committee desperate for validation.

They know the numbers stopped meaning anything. Belief fades like capital until there’s nothing left to mark.

Liquidity Theatre

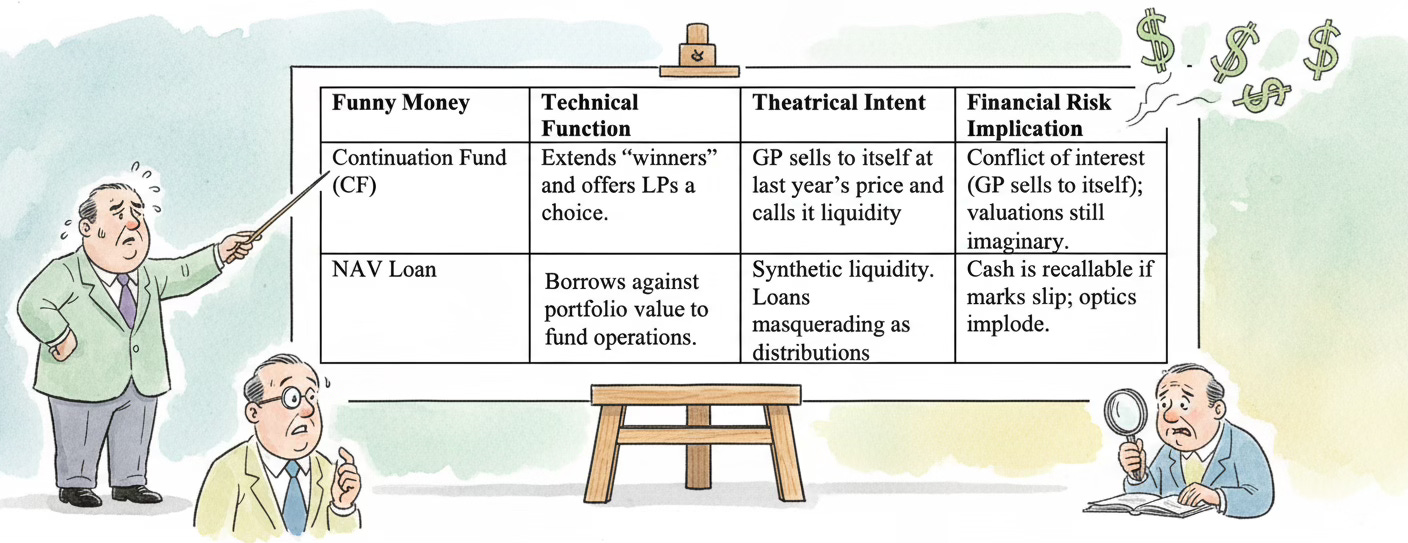

When the exits vanish, imagination becomes a liquidity strategy. This time it’s continuation funds, NAV loans, and single-asset vehicles pretending to be portfolios. They’re called liquidity tools, but they’re really stage props.

Continuation funds are the most convenient fiction. They claim to give LPs a choice: sell or stay, but in this market, they’re a survival mechanism. The GP plays both sides of the transaction, selling from one fund and buying into another, using its own valuation as truth. The price never gets tested. Assets move from one pocket to the next, the marks stay high, and everyone avoids the smell of an actual markdown.

General Catalyst6, Insight6, and Lakestar6 all opened continuation funds recently. The justification was liquidity; the subtext survival.

NAV loans are the other half of the act. Funds borrow against unsold assets and send the borrowed money back to LPs as “distributions.” It’s synthetic DPI: cash that looks like performance but comes from debt. The optics please committees and accelerate carry, but the money isn’t real in the way performance is real. If asset values slip and the covenants tied to those loans break, that cash can be recalled. The theatre collapses.

Together, continuation funds and NAV loans impersonate liquidity. The illusion works because everyone needs it to.

The pain of recognition is still worse than the cost of delay.

The Middle Distance

Between denial and surrender sits a long, gray hallway. Most portfolios live there. Too early for a funeral, too late for a victory lap.

This is how capital behaves when it can’t move forward or back. Portfolios start developing strange habits. Projections stretch, adjectives disappear, confidence gets formatted into bullet points. Nobody lies; they just stop finishing their sentences.

Markets like to call this discipline. It’s really drift. The slow adaptation to a world where nothing clears and everyone’s pretending that’s normal.

The Aftertaste of Abundance

Abundance leaves junk behind. Office leases that outlived morale. Data dashboards with nobody to read them. Rituals that made sense only when everything was sprinting uphill.

Founders still hold all-hands meetings to announce product pivots nobody asked for. Demo Days now feel like improv nights. Boards read metrics that measure activity instead of progress.

Abundance trained people to worship velocity. Now restraint feels like failure, so they simulate action. They call it iteration. They call it hustle. It’s just static.

Culture copies what it sees. The last generation won with spectacle, so the next one will try it again until it bankrupts them. No one tells them the music stopped three slides ago.

Administration of Pain

Markets heal through confession, not time. Confession costs too much, so they budget denial instead.

So, the pain gets bureaucratized. A markdown here, a process there, a quiet sale to a “strategic partner.” The wounds are managed, not treated. Everything happens in slow motion, so nobody gets blood on their term sheets.

There’s compassion in that, but also cowardice. Slow recognition keeps the peace while rot sets in. Teams that once built fast now specialize in holding ground. Entire vintages spend their prime years pretending not to notice entropy.

The system congratulates itself for stability. Stability is just decay with a consultant’s flourish.

What Remains

Markets shed illusions only when holding them becomes more expensive than letting go. Most of what passes for discipline is just exhaustion.

The habits that survive will be borne out of necessity. Funds will keep marking, founders will keep pitching, LPs will keep nodding. Not out of greed, but because belief is foundational.

What remains is interpretive dance. The reflex to keep pretending value exists somewhere just offstage.

The math endures because math doesn’t care. It doesn’t punish or forgive. It just reports.

Coda

Venture capital has become the joke it told about everyone else: a room full of self-styled innovators using spreadsheets as rosaries.

The deeper failure is belief, not valuation. The system didn’t lose its arithmetic; it lost its tolerance for it. The power law still works, it just stopped producing enough outliers to make the story hold. So narrative took over and called itself strategy.

That’s the final stage: survival through contraction. Cull the animals until the ecosystem is back to equilibrium. Call it discipline. Call it maturity. Call it whatever gets you through the quarter.

Recovery will come, but it won’t feel like redemption. It’ll feel smaller, quieter like an industry relearning how to live without applause.

Nothing failed. It just stopped working.

The challenge now is whether the industry can finally stop budgeting denial and start respecting the gravity it once claimed to defy.

References

National Venture Capital Association. (2025). NVCA 2025 Yearbook. Retrieved October 2025 from https://nvca.org/2025-yearbook/.

Stohl, Ryan, The Generalized Winner Constant (Wc): Structural Constraints Beyond Venture Capital (October 2025). Available at SSRN: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5599471.

Crunchbase News. (2024). The Complete List of Unicorn Companies. Retrieved October 2025 from https://news.crunchbase.com/unicorn-company-list/.

Crunchbase News. (2025). The Rise Of The Ultra-Unicorns: $5B+ Startups Are Leading The Private-Market Herd In 2025.Retrieved October 2025 from https://news.crunchbase.com/venture/ultra-unicorn-startups-lead-private-market-2025/.

Cambridge Associates. (2024). US PE/VC Benchmark Commentary: Calendar Year 2024. Retrieved October 2025 from https://www.cambridgeassociates.com.

Venture Capital Journal. (2025). Venture Secondaries and the Rise of Continuation Funds in Private Capital. Retrieved October 2025 from https://www.venturecapitaljournal.com/continuation-vehicles-are-accelerating-in-the-venture-industry/#.